How much profit a monopoly should earn is both an economic and a moral question. When it comes to growing our energy capacity and affordably, the best answer under our current energy system is that utilities should recieve enough get enough to get the job done -- but right now they are asking for a lot more.

While California customers face an affordability crisis, Investor-Owned Utilities are enjoying record-breaking profits two years in a row. Even still, these same utilities are asking the California Public Utilities Commission (CPUC) to increase their rates of return for shareholders, further squeezing the pocketbooks of their ratepayers. Clean energy is the most affordable option for customers and electrification will make our homes and businesses more efficient, and California has set ambitious decarbonization targets across multiple industries–-planning to spend billions of dollars on a clean energy transition. California’s utilities argue that they need higher profits to raise the capital necessary to build all that clean energy infrastructure, but they are motivated to maximize shareholder profits, not to uphold environmental values.

A clean energy transition will generate billions of dollars in benefits for Californians, but we all rely on the CPUC to make sure we’re not getting price gouged by the utilities in the name of progress. That's why the Sierra Club is pushing the CPUC to protect against corporate greed while ensuring the clean energy transition happens.

Utility Profits and Electricity Rates are Skyrocketing

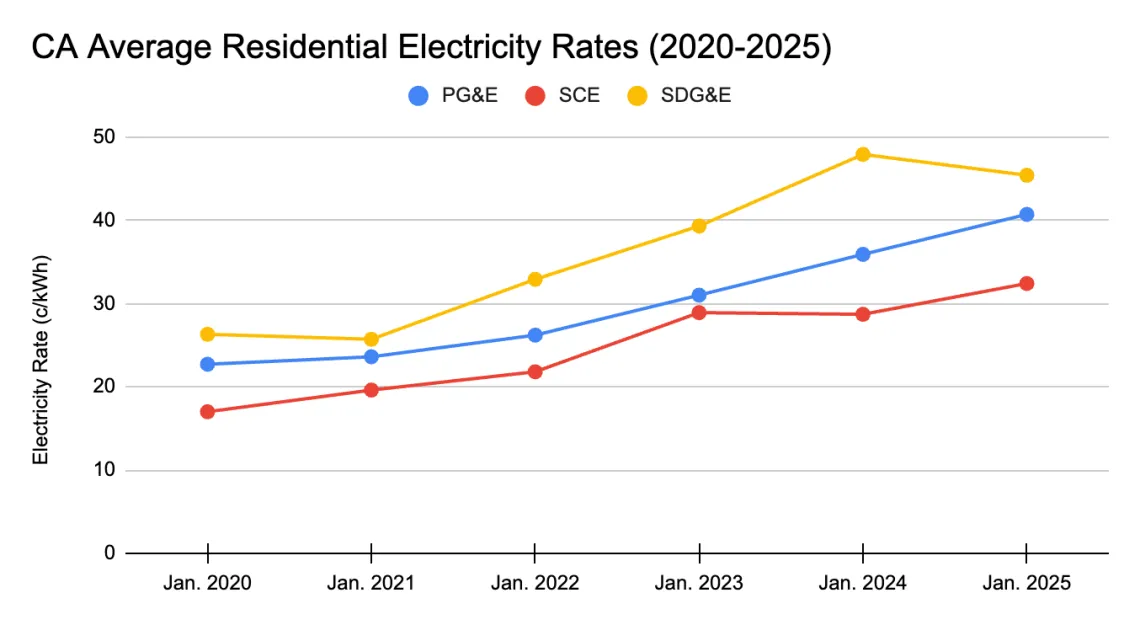

The three largest investor-owned utilities in California – PG&E, SCE, and SDG&E – all increased their residential rates an average of 13.3%, 12.3%, and 9.1% each year between 2020 and 2025, respectively (See Figure 1). Reasons for cost increases include expensive wildfire mitigation and increases in extreme weather events due to climate change, and utility lobbying. The CPUC faces tough choices in figuring out which costs to cut and how to save ratepayers money, like which programs merit continued funding as the budgets get crunched or how to spread costs across customer groups.

But one immediate tool at the CPUC's disposal is to decrease the amount of profit ratepayers pay to utility shareholders.

As many Californians struggle to make ends meet, utilities rake in record profits. In 2024 alone, PG&E made an unprecedented $2.47 billion in profits. This same year, the CPUC approved six rate increases for PG&E customers. SoCalEdison also made record profits of about $1.6 billion, almost a 10% increase from the previous year and San Diego Gas and Electric (SDG&E) made near-record profits of $891 million, following their record-breaking year of $936 million in 2023.

Furthermore, the legal standard for utility rates of return is to equal the cost of raising capital. Some finance experts argue that utilities have been asking for–and receiving–more returns than are actually necessary to raise capital. The burden is on the utilities to show how much it costs to raise capital, and public utility commissions are responsible for determining whether those requests should be approved. Commissions tend to approve those utility requests, but not always with sufficient scrutiny.

Rates-Of-Return for Shareholders

This year, yet again, utilities are asking for an increase in their Rate of Return (ROR) for shareholders. The Rate of Return is the percentage of profits, allowed by regulators, that a company can earn on its capital investments (i.e. building infrastructure, transmission lines, etc.).

Utilities’ argue they might not be able to attract capital if the rate of return is too low. However, investing in California utilities is a low risk investment, with nearly guaranteed cost recovery for utility investments especially for the three largest utilities in the state.

Moreover, there has been and will continue to be opportunities for returns on capital investments, as California needs major investments in clean energy and transmission infrastructure to meet its climate and renewable energy goals. With these continued investments, utilities stand to make billions of dollars in nearly-guaranteed profits.

This year, similar to previous years, utilities are asking for generous increases in Rates of Return. Sierra Club, in partnership with utility experts, is suggesting that utilities move to a more just and reasonable Rate of Return, which will still ensure shareholder profits and a good credit rating, while protecting ratepayers.

2024 Authorized Return on Equity and 2025 Proposed Return on Equity

Utility | 2024 ROE1 | IOU-Proposed 2025 ROE2 | Sierra Club-Proposed 2025 ROE2 |

Pacific Gas and Electric | 10.70% | 11.30% | 6.22% |

Southern California Edison | 10.75% | 11.75% | 6.11% |

San Diego Gas and Electric | 10.65% | 11.25% | 6.15% |

The CPUC Must Protect Ratepayers

The CPUC regulates utilities in California and has to decide the rate of return for utilities every three years. These regulators' job is to give the utilities a rate of return that will match the market cost of capital—no more and no less -- and to protect ratepayers. To stop the alarming trend of wealth transfer from ratepayers directly to corporate investors, we need to see regulators step up and defend everyday working people.

But in recent years they have repeatedly authorized increases in utility rates of return, at the expense of struggling families and businesses. State law and Supreme Court case law requires the CPUC to balance shareholder and ratepayer interests and to give the utilities a rate of return that will enable them to manage their responsibilities. The problem is that the Commission has never actually required the utilities to demonstrate how their requested rates support ratepayer interests, resulting in a clear and systemic bias towards shareholders’ interests. This has to change.

This year, California’s utilities argue that their cost to raise capital is 11%. In testimony, Sierra Club’s expert demonstrated that the long-term cost of capital is closer to 6% and that ratepayers’ interests are best served by setting lower rates of return, saving ratepayers $8.2 billion dollars compared to what the utilities request.

The CPUC will likely issue a decision by the end of this year. Sierra Club and our partners are urging the Commission to make a decision that benefits ratepayers, rather than lining the pockets of shareholders.

We are hopeful that the Commission will listen to communities that have been targeted again and again with unfair and irresponsible rate increases. We all deserve affordable electricity and the Commission has the power to take a step in the right direction by authorizing a lower rate-of-return for some of the wealthiest utilities in the world.

Figure 1

Graph shows the average rate increases from 2020-2025 for residential customers of CA’s three largest Investor-Owned Utilities. Note: Data shown here only represents January rates for each year. Rate calculations are based on 855 kWh/month Data from EIA Form 861M (monthly). Data from 2024 & 2025 are preliminary. Not all Utilities Report to EIA Form 861M.

Figure 2:

Data from filings at the California Public Utilities Commission.