Executive Summary

Introduction

Part 1: Why Investors Must Confront Climate Change as a Systemic Threat to Long-Term Portfolios

- The Climate Threat to the Economy and Retirement Security

- Why Investors Must Prioritize the Economy-Wide Impacts of Climate Change

- Why Conventional Sustainable Investing Fails to Mitigate Climate Change

- Investor Fiduciaries Have the Duty and Power to Reduce Climate Risk

Part 2: How Investors Must Deploy Their Leverage to Mitigate Systemic Climate Risk

- From Intent to Impact: The Mechanics of Investor Influence

- How Investors Can Use Their Levers of Influence to Drive Climate Action

- Aligning Values and Financial Impact

Conclusion: The Fiduciary Imperative for Climate Action

Acknowledgements

Disclaimer

Executive Summary

Climate change poses a growing threat to the global economy—and with it, to the retirement funds and long-term investments that millions of people depend on.

Yet traditional investing approaches—and even many sustainability-oriented strategies—focus narrowly on climate-related risks to individual companies’ profits, rather than the much greater threat climate change poses to the broader economy and the excessive damage that some companies cause. For those managing diversified investment portfolios, that approach is no longer adequate or responsible.

This paper makes the case that investors must treat climate change not just as a risk to individual companies, but as a threat to the entire economy and long-term portfolio returns. That kind of risk cannot be avoided just by trading assets or holding climate-friendly firms. Because market-wide climate damage comes from rising global emissions, the only way to reduce that risk is to reduce real-world emissions. That requires a strategic shift in investor behavior—from managing company-specific risk exposure to proactively mitigating systemic risk. Part 1 explains why this shift is necessary and urgent, and how conventional approaches—including ESG integration and shareholder divestment—fall short.

Part 2 outlines what investors should do instead. It emphasizes that meaningful impact depends on how different forms of capital—particularly debt and equity financing, across primary and secondary markets—shape investor leverage. It details how four key levers should be deployed: directing capital, engaging with companies, supporting strong public policy, and holding financial intermediaries accountable. By strategically using these tools together, investor fiduciaries can fulfill their responsibilities to safeguard portfolio value by driving real-economy decarbonization and strengthening market-wide stability.

Introduction

If you care about action on climate change or protecting your retirement savings—or, like most people, both—you should care about how our investment system works, because it threatens them both.

Traditional investing seeks to grow returns by encouraging each company in a portfolio to maximize its own profits. But that approach breaks down when some companies create risks that threaten the health of the economy—and with it, long-term portfolio value. This is especially true for diversified portfolios, such as pensions and retirement funds, which depend far more on the strength of the broader market than on the performance of individual firms.

Most people experience the market in fleeting snapshots—daily headlines, quarterly reports, temporary dips and rallies. But their investments are meant for much longer horizons. If you contribute to a 401(k) or pension each month, that money likely won’t be accessed for decades. That’s why the standard advice is to diversify and ride out the highs and lows. And in recent decades, that’s generally worked—the market has recovered from downturns and kept climbing. But continued growth rests on a critical assumption: that the environmental and social systems underpinning economic activity will remain resilient and intact. Increasingly, that assumption is untenable in the face of climate change.

Imagine a public school teacher early in their career today, contributing to a pension fund and expecting it to grow steadily over time. They may not retire for 30 years—by which point the impacts of escalating global warming are projected to severely reduce global stock values. That damage is driven largely by a small number of corporate polluters. When companies boost profits by offloading the costs of their pollution onto society, they erode the systems on which the economy and financial markets depend.

Investors can’t avoid these risks by diversifying their holdings, which is how they typically manage risks to particular companies. Unless emissions are cut, portfolios will bear the consequences. That’s why, for most investors, combating climate change shouldn’t just be an ethical concern—it’s a financial imperative. Yet traditional investment strategies remain focused on maximizing company-by-company profits. And even conventional sustainable investing follows the same logic—avoiding risks to individual firms, rather than confronting the broader harms that some cause.

These approaches often rely on the hope that corporate profits naturally align with sustainability, and that investors will benefit simply by holding “greener” companies. While that “win-win” logic may hold in some cases, it breaks down for major polluters whose business models rely on unchecked emissions. Unless those companies are forced to change and emissions are slashed, the consequences for the broader economy—and for most long-term investors—will worsen.

When government oversight weakens and corporate pledges falter under political pressure—as is happening now in the U.S.—investor action becomes even more urgent. If climate progress slows, the financial fallout will only deepen. Protecting the health of the economy from climate breakdown is in investors’ best interest, even when those actions conflict with some companies’ short-term incentives. It’s time for more investors to confront that reality—and act accordingly.

Part 1: Why Investors Must Confront Climate Change as a Systemic Threat to Long-Term Portfolios

Climate change is not just an environmental crisis—it is an accelerating threat to the global economy and the investment portfolios that millions rely on for financial security. Rising greenhouse gas emissions are already causing widespread damage, undermining economic stability and long-term growth. Without major emissions cuts, we risk crossing dangerous planetary thresholds that will lead to staggering financial losses.

Climate change already causes hundreds of billions of dollars in damages each year. On our current trajectory, the global economy could face annual losses exceeding $38 trillion by mid-century—and the toll could grow far worse later in the century. These costs—from extreme weather, infrastructure damage, supply chain shocks, reduced labor productivity, and more—already strain economies and far exceed the projected costs of cutting emissions. In the U.S., growing climate-driven instability in insurance and mortgage markets is an early warning of broader economic disruptions.

As warming disrupts ecosystems and societies, it also exacerbates other economy-wide threats—including deepening economic inequality, accelerating biodiversity loss, and increasing the risk of pandemics. These compounding crises strain markets and make climate change a defining economic challenge of our time.

The consequences extend to retirement funds: unchecked climate change could slash global stock values by 40% by mid-century—or possibly over 50%, if tipping points like the collapse of the Amazon rainforest or polar ice sheets are triggered. These losses are unlikely to be temporary; they could become enduring drags on investment returns, especially for retirement funds and other long-term portfolios.

For countless people, the financial impacts of climate change could be devastating—potentially “comparable to the damage caused by the 1929 Great Depression, but experienced permanently.” While these risks may feel distant, they fall well within the working years of today’s adults, and will define the future of today’s children and following generations.

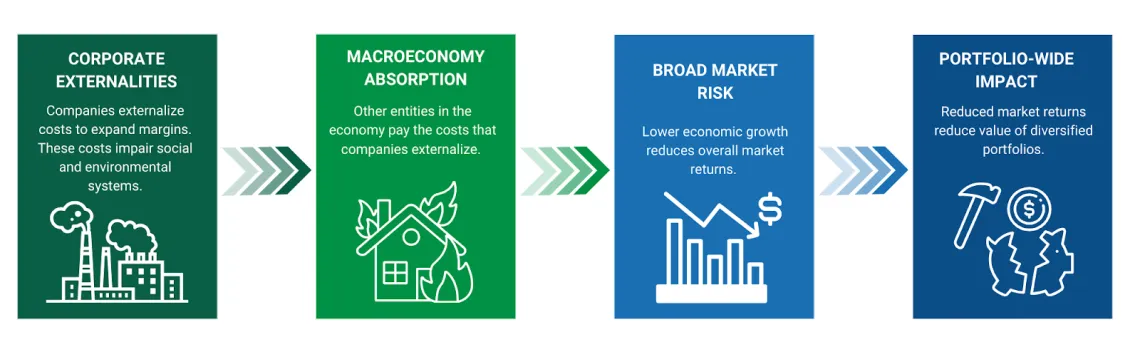

Figure 1.1: The externalized costs of companies’ greenhouse gas emissions flow through the economy, slowing growth and reducing the long-term returns of diversified portfolios. Credit: The Shareholder Commons

The warnings are clear: climate breakdown leads to economic and financial breakdown. Combating climate change is essential not only to safeguard ecosystems and promote justice, but to protect the global economy and investors’ long-term financial security.

Despite mounting evidence, many investors still underestimate climate risks. This is partly due to political pressure and disinformation from corporate polluters—especially in the U.S.— that have worked to halt financial sector climate action. But an underlying problem lies in the widespread reliance on economic models that systematically understate climate risks. These models often ignore tipping points, feedback loops, and non-linear impacts, creating projections that offer a dangerously false sense of security.

Some investors still call for more precise data before acting. But waiting for perfect information becomes an excuse for further delay while real-world consequences escalate. A more prudent and responsible approach requires acting now to prevent much greater damage.

As climate instability worsens, it will erode economic growth, weaken market-wide performance, and undermine the value of diversified portfolios. Yet many investors still treat climate change primarily as a risk to individual companies—managing it by diversifying holdings, avoiding riskier firms, or supporting emissions cuts only when profitable for that firm.

But climate change is not just a risk to companies—it’s a threat to the global economy, driven disproportionately by a small group of corporate polluters. A company’s emissions don’t just affect its own performance—they contribute to broader economic damage that harms diversified portfolios. Stock picking and firm-level risk management cannot shield portfolios from that reality.

Understanding climate change as a system-wide financial threat reveals an unsettling truth: traditional investing strategies—including many labeled as “sustainable”—are not designed to mitigate the economy-wide impacts of the climate crisis on most retirement funds. Focusing narrowly on firm-level risks obscures the far greater threat to entire markets.

Although global temperatures have now surpassed the 1.5°C mark —long recognized as a critical threshold—every fraction of a degree in additional warming still matters enormously to save lives, protect ecosystems, and avoid massive financial losses. Reducing emissions is essential to stabilizing global markets, strengthening long-term growth, and safeguarding people’s life savings.

In summary: Climate change poses a massive and growing threat to the global economy and long-term investment performance. Yet many investors still underestimate its scope, relying on outdated models and narrow frameworks. The only way to meaningfully reduce the financial threat is to reduce economy-wide emissions.

The climate-related risks faced by individual companies are substantively different from the system-level risks that climate change poses to the broader economy and diversified portfolios. While the phrase “climate risk is financial risk” is now widespread, it’s essential to distinguish between different types of risk, how they manifest, and how to respond effectively.

Company-specific risks (also called idiosyncratic risks) are challenges such as product failures, supply chain disruptions, or market shifts that affect a firm’s financial performance. Climate change can cause or amplify these risks through physical impacts, like extreme weather, and transition-related changes, such as new regulations or shifting consumer demand. These risks can be significant, and most investors seek greater transparency into how firms manage them.

By contrast, system-level risks (also called systemic or systematic risks) are economy-wide threats that cut across sectors, and cannot be avoided or mitigated by diversifying investment portfolios. These issues threaten overall economic stability, not just individual firms’ performance—requiring proactive efforts to address their root causes. The projected 40% hit to global stock values by 2050 illustrates the magnitude of systemic climate risk.

Systemic Risk Should Be a Top Concern for Most Investors

The greater concern for most investors shouldn’t be how individual companies cope with climate-related risks, but the broader economic fallout of unchecked climate change itself. Treating climate change primarily as a company-specific issue overlooks how some firms profit by externalizing the costs of their emissions onto society. These firms may perform well in the short term even as they destabilize the economy and erode long-term portfolio value. Focusing on systemic risk makes clear why investors have a financial interest in accelerating climate action—regardless of whether certain companies feel pressure to change.

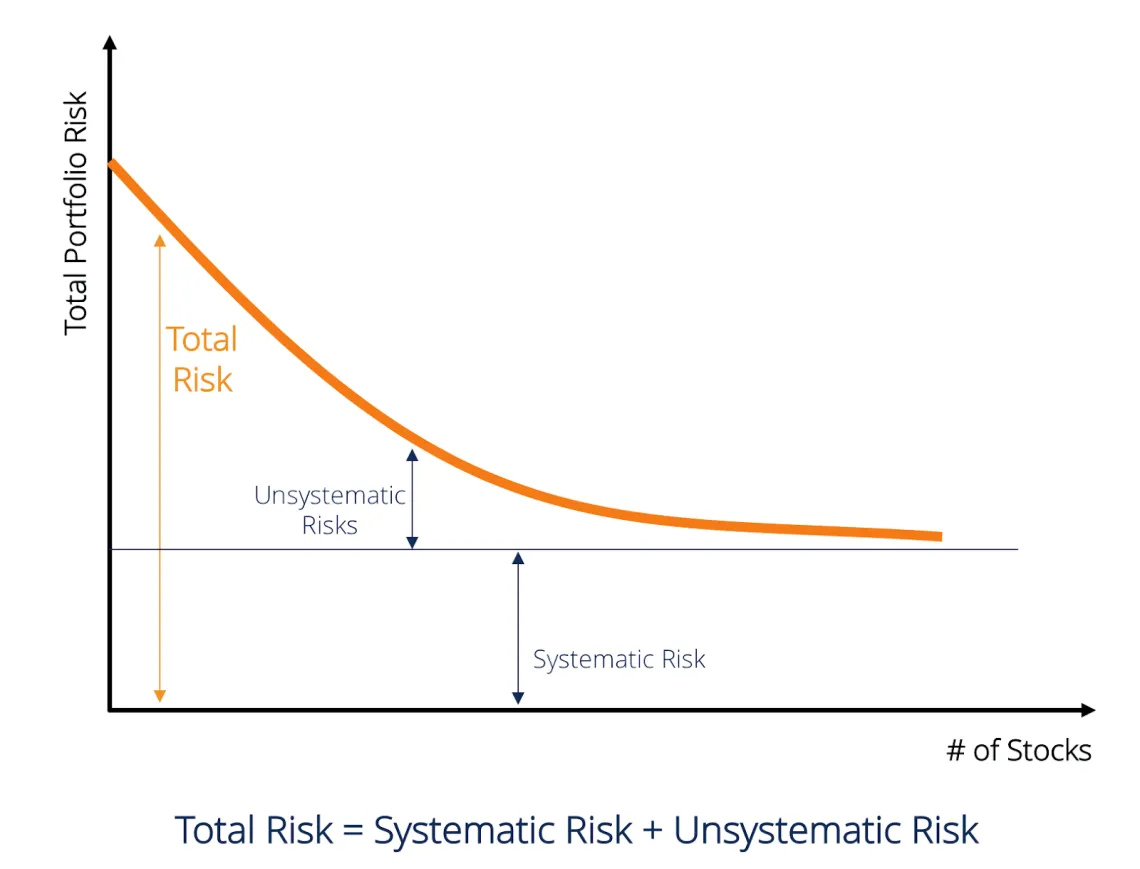

Crucially, studies show that 75% to 94% of the variability in diversified portfolio returns is explained by exposure to broad market forces—not by picking outperforming assets. In other words, most portfolios’ performance depends far more on the overall health and stability of the market than on individual investment choices or the performance of particular companies.

Consider the stark contrast between transition risks to some major polluters and the broader financial toll of inaction. For example, stranded fossil fuel assets are often cited as a risk if the energy transition happens rapidly. But even if countries meet their current climate pledges—which most are not on track to do— the global cost of stranded fossil fuel assets is projected to total $2.3 trillion by 2040. That’s comparable to the cost of climate disasters over the past decade —and only a fraction of the tens of trillions in annual losses projected if emissions remain unchecked. Transition risks may deeply affect certain companies, but the greater financial threat for most investors lies in the systemic consequences of inaction.

Managing firm-level risks is still important—especially as physical and transition threats can materially affect businesses. But these measures only address risks to individual holdings—not the market-wide forces that shape most long-term portfolio performance. Diversification can help with firm-specific risks, but it can’t shield portfolios from climate-driven systemic threats. These risks are unavoidable and must be addressed at their source.

Traditional Investing Does Not Address Systemic Risk

Traditional investing emphasizes broad diversification and assumes each company will maximize its own profits. The premise is that gains from some companies will offset losses from others, thus balancing risk and return over time. This model underpins most long-term portfolios—such as 401(k)s, IRAs, and pensions—often held through mutual or index funds diversified across thousands of companies. While some investors may outperform benchmarks, like the S&P 500, through stock picking, portfolio returns over time tend to be stronger when investing broadly. That’s why many large investors have highly diversified portfolios and are referred to as “universal owners”—reflecting their exposure to the global economy.

Figure 1.2: As portfolios diversify, company-specific (unsystematic) risk declines, leaving market-wide (systematic) risk as the main driver of long-term portfolio risk and performance variability. Credit: Corporate Finance Institute

But traditional investing assumes that if every company maximizes its profits, portfolio performance will follow. That logic fails when companies profit by offloading costs—like greenhouse gas emissions—onto broader society. In some cases, those byproducts cause systemic damage to entire markets. Addressing systemic risk doesn’t require rejecting profit—it requires guardrails to ensure corporate profits aren’t generated in ways that undermine long-term economic stability.

Traditional investing also overemphasizes benchmark-relative performance. For instance, a fund manager might be praised for losing only 8% in a market that fell 10%—or penalized for gaining 8% when the market rose 10%. This narrow focus obscures the fact that for diversified investors, what matters most isn’t relative performance—it’s how well the entire market performs over time.

Because diversified portfolio performance is largely shaped by market-wide conditions, investors will remain exposed to escalating losses unless emissions decline rapidly. Simply decarbonizing portfolios—shifting investments toward companies with lower emissions—won’t solve the problem. What matters is cutting emissions in the real economy—where goods are produced, services are delivered, and climate damage is generated. That's where action to mitigate systemic climate risk must take place.

To protect long-term value, investors must address the root causes of climate risk—especially the outsized damage caused by high-emitting companies. Yet many climate-focused strategies still prioritize “portfolio decarbonization” over real-world impact—holding firms with lower reported emissions or stronger sustainability scores, even when these choices don’t reduce actual emissions. This disconnect between portfolio optics and real-economy outcomes highlights the limits of conventional sustainable investing practices.

In summary: Climate change is not just a risk to individual companies—it is a systemic threat to global economic stability and long-term portfolio value. In diversified portfolios, overall market trends are the primary driver of long-term performance—which cannot be safeguarded through firm-level risk management alone. To mitigate systemic climate risk, investors must go beyond firm-level risk management and take action to reduce real-economy emissions.

Many investors have adopted strategies they consider climate-conscious. But rather than addressing how companies contribute to the climate crisis, most remain narrowly focused on how climate-related risks might affect individual firms’ short-term profits. As a result, these strategies often fail to reduce the real-world emissions driving systemic climate risk—and may even reinforce the narrow, short-term thinking that leaves portfolios more vulnerable.

The Limits of Voluntary Corporate Climate Action

Most companies have little reason to reduce emissions purely in response to climate-related risks they face themselves—especially if their competitors don’t. Cutting emissions can be costly, while the benefits of a safer, more stable climate are shared across the economy. That’s why climate change is called a “tragedy of the commons”: companies are often rewarded for prioritizing their own profits, even when their emissions harm the entire economy. Changing this dynamic requires strong external pressure—from public policy, competitive forces, and investors themselves.

Too often, companies delay meaningful climate action or take only superficial steps—such as promoting dubious carbon offsets, issuing vague pledges, or making misleading sustainability claims—while continuing to pollute. Worse, many major polluters have spent decades lobbying for subsidies and against climate policies to protect their profits and avoid regulation.

Even well-intentioned companies often prioritize protecting short-term profits over reducing emissions. They may address physical risks by relocating facilities, reinforcing infrastructure, or diversifying supply chains. They might manage transition risks through efficiency measures or carbon offsets. But companies rarely cut emissions beyond what’s required—unless compelled by regulation, market demand, or investor pressure. This reflects a deeper reality: sustainability improvements and narrow profit maximization often diverge—especially when companies can pollute freely—and that divergence ultimately harms the economy and investors.

The fact is that the urgency of transition risks depends on the pace of the transition itself. When regulation weakens or clean energy adoption slows, high-emitting firms face less pressure to decarbonize—and more incentive to stick with emissions-heavy strategies that deliver short-term profits. But this delays the transition, accelerates climate damage, and deepens systemic risks to markets and portfolios. The result is a dangerous feedback loop: as climate action stalls, companies may double down on polluting business models—intensifying the very threats that diversified investors cannot escape.

Much attention has been paid to the risk of stranded fossil fuel assets if the energy transition happens rapidly. But the far greater danger is failing to act fast enough—allowing systemic risks to escalate while short-term pressures to decarbonize diminish. When climate policy weakens or market signals fade, firms have further incentive to double down on high-emitting business models, worsening the long-term damage to markets and portfolios.

By fixating on short-term company-level risks, investors may inadvertently contribute to delay—discouraging action just when it’s most needed. In some cases, this mindset even leads them to oppose government policies or corporate reforms that would reduce emissions—prioritizing near-term gains over long-term economic stability. But doing so ignores the reality that systemic risk poses a far greater threat to diversified investors than the performance of particular companies.

High-emitting companies often create a sharp misalignment for diversified investors: their short-term profits come at the expense of the long-term strength of the broader economy and most portfolios. This is especially true in sectors like fossil fuels, utilities, and heavy industry, which produce the vast majority of global emissions. The fossil fuel industry is the clearest example: its core business—extracting and burning coal, oil, and gas—is the single largest driver of global warming. Managing the risks that climate change poses to these companies individually is fundamentally different from addressing the systemic risks they create for the broader economy.

That’s why systemic risk mitigation can’t be left to company discretion—it requires sustained pressure and alignment from governments, consumers, and investors. A firm can protect its own bottom line while worsening systemic risks that threaten diversified portfolios. This creates a critical disconnect: without sustained accountability from regulators and investors, profitable but harmful practices will persist—imposing massive costs on the broader economy.

Voluntary corporate action is not enough to mitigate systemic climate risk. Companies are already incentivized to prioritize short-term profits, and shifting political and market conditions often reinforce that focus. For investors, reducing economy-wide emissions—not just avoiding risky firms—is essential to safeguarding long-term value.

The Limits of ESG Investing and Shareholder Divestment

Common sustainable investing strategies today are constrained by the same assumptions that underpin traditional investing. Many proponents are deeply concerned about the climate crisis, but the strategies themselves focus on firm-level risk exposure rather than addressing the structural forces driving systemic risk. While investors once largely ignored companies’ environmental, social, and governance (ESG) issues, ESG integration is now a mainstream tool for evaluating sustainability risks that were traditionally overlooked. It is often framed as a sustainable alternative to conventional investing, but in practice ESG integration functions largely as a traditional risk management tool that considers a broader range of factors.

ESG ratings primarily assess how well companies manage risks to their own operations—not the broader impacts they impose on society or the environment. These metrics largely overlook firms’ externalities—like greenhouse gas emissions—that drive systemic financial risks. In essence, ESG ratings don’t “measure the impact of a corporation on the world; it’s all about whether the world might mess with the bottom line.” While debates continue over whether ESG-rated companies or investment funds outperform their peers, one thing is clear: ESG strategies were not designed to address corporate externalities or mitigate system-level risks, and thus are poorly suited to mitigating a threat like climate change.

For example, a company that bulldozes a rainforest and displaces an Indigenous community may receive a lower ESG score—but only; due to the potential legal or reputational penalties that could ensue, not the actual harms to the environment and human rights. And because ratings are generally relative within an industry, a company may receive a higher score simply for disclosing its risk management strategies—even if its practices remain harmful to the environment, communities, and the health of the broader economy.

Rather than prompting a reckoning with these structural limitations, much of the public debate around ESG has become distorted—distracting from the urgent need to address economy-wide risks. Many sustainability advocates raise sincere concerns about greenwashing, calling out how ESG funds often include holdings in major corporate polluters. Meanwhile, corporate polluters and their political allies have launched bad-faith attacks and disinformation about “ESG” in order to undermine climate-conscious investing altogether.

Though these critiques come from opposite sides, both miss the core issue: ESG is a firm-level tool designed to assess how sustainability risks affect corporate performance—not how companies contribute to systemic risks like climate change. That’s why the inclusion of fossil fuel companies in many ESG funds should be understood not as a failure of execution, but rather as a reflection of ESG’s narrow purpose.

Similarly, shareholder divestment—including avoiding or selling shares of particular publicly traded companies—follows the same firm-level logic as ESG integration. While often motivated by serious concerns about global climate damage, shareholder divestment primarily serves to limit an investor’s exposure to potential losses if a specific company or sector declines in value. That may help reduce firm- or sector-specific risks within a portfolio—but it does little to address the broader economic consequences that those companies contribute to through continued emissions.

Even if, for example, fossil fuel companies ultimately suffer transition-related losses—including major write-downs or stranded assets—the systemic risk posed by unmitigated climate change is a far greater threat to the overall market and to diversified portfolios. Selling or avoiding shares may sidestep some exposure to company-specific risks—but it neither mitigates the harm those companies inflict on the broader economy, nor avoids the market-wide fallout of accelerating climate damage.

Both ESG integration and shareholder divestment assume that protecting portfolio returns means managing exposure to individual companies—rather than confronting how those companies shape market-wide conditions. But for diversified investors, the health of the overall economy matters far more than the profits of particular companies or sectors. Protecting long-term portfolio value requires investor action that reduces real-economy emissions—not just reshuffling holdings or pushing companies to guard their own profitability.

When regulatory or market pressures mount, investors may press companies to reduce emissions. But when those pressures ease, so does the incentive to act—allowing carbon-intensive practices to continue and systemic risk to grow. Deregulation only deepens this problem by delaying transition risks and giving polluters more freedom to pursue short-term profits at the expense of long-term stability.

Political winds and market signals may shift—but what remains constant is that unless emissions decline, economy-wide climate damage will escalate. For investor fiduciaries, the goal must be not just to avoid climate risks, but to actively reduce them.

In summary: Conventional sustainable investing tools like ESG integration and shareholder divestment focus on managing exposure to specific companies, not on mitigating the structural causes of systemic climate risk. These approaches may reduce firm-level risks, yet leave portfolios exposed to the much greater damage caused by rising emissions. Protecting long-term value requires investor strategies that confront and reduce the drivers of climate breakdown.

For investor fiduciaries—those legally entrusted to manage others’ money—protecting long-term portfolio value requires more than managing company-specific risks. It means confronting the system-wide financial threat of climate change by taking action to reduce the real-world emissions that drive it. The financial security of millions of people depends on it.

Addressing Systemic Risk Is a Fiduciary Imperative

Many investors who acknowledge climate risk still assume they can’t address it directly. They focus narrowly on how companies manage their own risks, overlooking the broader economic damage some firms cause. But for diversified investors, long-term portfolio performance depends far more on overall economic health than on the success of particular firms. Ignoring system-level threats like climate change leaves portfolios exposed to deeper, market-wide losses.

Investors are not powerless in the face of system-level risks; nor do they need to sacrifice returns to take action. The outdated belief that markets are immutable—and that companies will voluntarily align with long-term economic health—has left many investors unprepared for some of the defining challenges of this century.

In reality, investors—especially large institutions—have significant influence over the real economy in the ways they allocate capital, engage with corporations, and advocate for policy reforms. Given their diversified portfolios and long-term obligations, institutional investors like pension funds have the incentive and the obligation to act.

Investors cannot rely on governments or companies alone to lead—especially as political and market pressures often shift. High-emitting firms typically respond to transition risks only when those risks feel imminent. But when regulatory and market signals weaken, companies face less pressure to act, and investors may misread that as a decline in risk. In reality, as emissions go up, the larger threat of climate change keeps escalating—and the longer the delay, the greater the long-term financial damage.

To protect diversified portfolios, investors must proactively support real-economy decarbonization. Strategies that rely on ESG ratings or focus only on avoiding polluters may manage company-specific risks, but they do little to address the broader instability caused by rising emissions. Mitigating systemic risks like climate change is not an optional add-on—it’s central to fiduciary responsibility.

Asset Owners Must Lead on System-Level Action Large institutional investors are often called “universal owners” because they hold broadly diversified, long-term portfolios that are exposed to economy-wide risks. But it’s important to distinguish between two types of actors in this system: asset owners and asset managers. Asset owners—such as pension funds, sovereign wealth funds, university endowments, and foundations—have legal ownership of their capital and are responsible for setting long-term investment priorities. Because their portfolios depend on broad economic stability, reducing systemic risks like climate change is essential to protecting and strengthening long-term value. Asset managers—such as BlackRock, Vanguard, State Street, and Fidelity—are hired by asset owners and individuals to manage their investments. These firms operate on a fee-based model, prioritizing client recruitment and retention to maximize assets under management. Their accountability centers on managing individual asset performance—not on safeguarding market-wide outcomes. Unless asset owners explicitly direct them to address systemic risks like climate change, most asset managers default to conventional strategies focused on company-specific risks. That’s why asset owners are pivotal in the shift toward systemic risk mitigation. Asset managers take their cues from the priorities—explicit or implied—of their clients. Unless asset owners clearly instruct their asset managers to mitigate systemic climate risk, most asset managers will simply stick to conventional investing strategies. To fulfill their long-term obligations, asset owners must set clear mandates, actively monitor execution, and hold asset managers accountable. If necessary, asset owners can move their investments to other asset managers. |

Fiduciary Duties Demand Climate Action

Fiduciary duties—established under federal and state law—require those managing others’ money to act in the best financial interests of clients and beneficiaries. This includes both asset managers, who are hired to oversee specific funds, and asset owners—like pension fund boards—who are responsible for the long-term health of the full portfolio.

Core principles that define fiduciary duty include: the duty of loyalty, which requires fiduciaries to put clients’ or beneficiaries’ interests above all else; and the duty of care, which demands informed, diligent, and prudent decision-making. For long-term investors, this means actively assessing and addressing systemic risks like climate change.

Fiduciaries also have a duty of impartiality to balance the interests of current and future beneficiaries. Public pension funds, for example, are accountable to millions of workers—like teachers, firefighters, and other public servants—who rely on the pension for their retirement security. Pension trustees are responsible for both retirees drawing benefits today and for younger workers relying on those same funds decades from now. Prioritizing short-term returns at the expense of long-term portfolio health risks shifting costs onto future generations. As previously noted, current warming projections could lead to a 40% hit to global stock values by mid-century—before many people in today’s workforce are set to retire, with even greater risks looming for today’s children and future generations.

Fulfilling fiduciary duties requires continuous learning and responsiveness to changing economic realities. Failing to act on major, well-known risks like climate change could jeopardize portfolio value—and potentially breach fiduciary obligations. As responsible investing has evolved, so too has the legal understanding of fiduciary duty. It is now widely recognized that fiduciaries must address sustainability risks—especially when they pose significant threats to portfolio returns. A major recent analysis of legal standards around the world, including in the U.S., affirmed that fiduciaries not only can, but must, act on sustainability risks that affect markets and long-term portfolio value.

Traditional investing assumes that if every company maximizes its profits, portfolio performance will follow. But when some firms profit by externalizing costs—like carbon emissions—that cause economy-wide losses, that logic falls apart. Managing or avoiding company-specific risks doesn’t address systemic threats to the broader market. Companies that drive these systemic risks may deliver short-term gains, but their broader impact harms diversified investors. For fiduciaries, mitigating such risks is essential to protecting portfolios—even if that challenges the narrow interests of some firms.

Ultimately, fiduciaries have a responsibility to help safeguard their clients’ and beneficiaries’ financial security. Addressing systemic risks like climate change is not about politics or social values—it’s about protecting and improving economic performance. By adopting the strategies outlined in Part 2, investor fiduciaries can better fulfill their obligations by contributing to a more secure and sustainable financial future.

In summary: Investors have both the power and the legal duty to address climate change as a system-level financial risk. For institutional investors—including asset owners like pension funds—this is not optional: the success of their long-term portfolios depends on the health of the broader economy. Fulfilling that duty requires more than stock picking and managing company-specific risks. It demands using their influence to reduce the real-world emissions driving the climate crisis—and to protect the financial well-being of both current and future beneficiaries.

Part 2: How Investors Must Deploy Their Leverage to Mitigate Systemic Climate Risk

Part 1 explained why investors must confront climate change as a system-level financial threat—not just manage company-specific risks. Climate change threatens the value of diversified portfolios and can’t be addressed through stock picking or firm-level risk management alone. Traditional investing strategies—including many labeled “sustainable”—were not designed to reduce real-world emissions or mitigate systemic risk. For investor fiduciaries, addressing this threat isn't optional, it’s essential.

Part 2 turns from why to how. To protect long-term portfolio value, investors must prioritize strategies that drive real-economy decarbonization—not just decarbonize investment portfolios. This shift is critical to confronting the climate crisis and the economic disruption it threatens. Investors can and should use their full range of influence to advance climate action now.

Key Indicators of Investors’ Real-Economy Impact

Because financial actions are difficult to directly trace to emissions reductions, investor influence is best assessed through “transmission mechanisms”—the pathways by which investors influence corporate behavior and market outcomes. These mechanisms apply across different types of leverage and financing, and can be assessed through three key indicators: corporate behavior, cost of capital, and access to capital.

Corporate behavior change is the most direct measure of investor impact that leads to real-economy emissions reductions. Investors can influence corporate strategy, governance, and operations—pushing firms to adopt targets, shift capital expenditures, or change leadership priorities. This influence flows through engagement, financing terms, regulatory pressure, market demands, and public expectations. Since behavior changes can take time, financial signals play a critical role in guiding strategy decisions—making polluting activities less attractive while supporting climate solutions. Two crucial financial levers are cost of capital and access to capital.

Cost of capital, or the return investors require to provide financing, determines how expensive it is for companies to raise funds. Higher costs for polluting projects can make them less financially viable, while lower costs for clean energy projects can improve their competitiveness and scalability. This dynamic can shift corporate strategies, even for firms resistant to other forms of engagement. In capital-intensive sectors—like energy—that need frequent financing, investors have especially strong leverage to drive change.

Access to capital refers to whether companies can obtain financing in the first place, regardless of cost. Even if firms are willing to pay more, they may be unable to secure funding if investors or lenders restrict capital for certain polluting activities. When capital is withheld due to financial institutions’ policies, capital-intensive business models can become less viable. Conversely, expanding capital access for clean energy—especially for emerging players and new markets—can accelerate the clean energy transition by supporting growth and innovation. Investors seeking long-term climate stability must be willing to provide stable, long-term financing to support it.

Investors can drive decarbonization by influencing corporate behavior, the cost of capital, and access to financing. These mechanisms are interconnected: even when companies resist change, investor actions that make highly polluting activities more expensive—or cutting off financing entirely—can promote business model shifts and reshape markets. Just as importantly, increasing investment and lowering capital costs for climate solutions can accelerate their deployment and strengthen their viability. By targeting these indicators, investors can accelerate emissions reductions and reduce systemic climate risk in order to protect long-term portfolio value.

Investors Need a System-Level Approach to Tackle Climate Change

To reduce real-world emissions and systemic risk, investors must adopt a system-level approach that strategically redirects financial flows, shifts corporate behavior, and shapes public policy. This requires effective use of four key levers: capital allocation, investment stewardship, policy advocacy, and service-provider accountability. Tailoring strategies to the structure of financial markets—especially differences between debt and equity, and between primary and secondary markets—is essential to targeting actions where investor influence is most direct and powerful. System-level investing ensures that financial tools are applied across asset types and decision points to maximize real-economy impact.

One example of this approach, used by some institutional investors, is summarized as “deny debt, engage equity.” In the energy context, this refers to restricting debt financing for fossil fuel expansion, while using equity ownership to drive stronger corporate accountability. This reflects two core principles: (1) limiting debt financing can constrain high-emitting activities in industries that rely heavily on debt; and (2) active stewardship by shareholders can maintain pressure and accelerate corporate transition plans across sectors pivotal to the low-carbon transition. This strategy is broadly applicable to other high-emitting capital-intensive sectors, as capital allocation is most influential when companies are raising new funds—most often through debt.

Focusing on these dynamics moves beyond the narrow debate over shareholder divestment versus engagement —which tends to overlook how the energy sector is financed and where investors have the most leverage. Because fossil fuel companies rely much more heavily on new debt than equity, denying debt can be more impactful than selling shares, which often transfers ownership to less climate-conscious investors. While restricting new equity financing can also be impactful, debt remains the more critical leverage point, as it accounts for the vast majority of the sector’s funding.

But holding polluters accountable is only part of what system-level investing demands. Investors must also scale up capital for climate solutions to reduce systemic risk and drive long-term growth. Expanding; investment in clean energy deployment, electrification, efficiency, energy storage, grid optimization, and climate resilience is also essential to cut emissions and protect portfolios.

The next section outlines how investors can use each of their four key levers to influence real-economy outcomes and reduce systemic climate risk.

To reduce economy-wide damage, investors must focus on real-world emissions—not just managing company-specific risks. That means using financial influence strategically across four key levers: capital allocation, investment stewardship, policy advocacy, and service-provider accountability. Each lever functions independently, but they are most effective at shifting incentives, redirecting capital, and enforcing accountability when used together. The impact of capital allocation and stewardship in particular depends on how they’re applied across different investments, sectors, and market structures. By aligning these strategies with how financial markets actually work, investors can maximize leverage and better mitigate systemic risk.

How Market Structures Shape Investor Influence

To drive real-economy decarbonization, investors must focus on how companies raise and manage capital—since financing structures determine where leverage is strongest. Two distinctions are especially important: debt vs. equity financing and primary vs. secondary markets. These shape how capital reaches companies and what types of investor actions are most effective.

Other investment categories—especially private equity and credit markets—are becoming more prominent, with pension funds and other asset owners increasing allocations. While shareholder voting is less applicable in private markets, investment decisions there can still drive real-economy change. Nonetheless, public equity and debt markets remain the most prominent channels through which institutional investors influence major corporate emitters.

Figure 2.1: Companies raise capital by issuing bonds to investors (with banks facilitating the sale) and repaying the debt over time with interest. Source: Sierra Club |

Figure 2.2: Companies raise equity capital by issuing shares (with banks facilitating the sale) to investors, who become partial owners with voting rights. Source: Sierra Club |

Debt vs. equity financing

Debt financing, including bonds and loans, requires companies to repay borrowed capital with interest. Unlike equity, which is often issued only once or infrequently, debt must be repaid and reissued on a regular basis. This time-bound structure makes debt markets especially powerful for shaping corporate behavior, as companies must routinely return to them for refinancing—often with terms that reflect lenders’ views on long-term risks.

Equity financing involves issuing stock (or shares), giving investors ownership stakes in a company. Unlike debt, equity does not require repayment, but in the case of public companies, provides shareholders governance rights—such as voting on corporate boards and shareholder resolutions.

Most companies issue new equity infrequently—often just once during an initial public offering (IPO)—though some may raise additional equity later. While equity markets tend to have fewer intervention points than debt for shaping a company’s ability to raise capital, shareholder advocacy and voting can still influence corporate behavior on an ongoing basis.

Primary vs. secondary markets

Primary markets are where companies raise new capital through bond or stock issuances and bank loans. Investor decisions at this stage directly affect a company’s ability to fund operations, scale projects, or transition business models.

Secondary markets involve trading existing stocks and bonds between investors. Buying these assets does not provide companies with new funding, and selling does not take money away—though such trades can influence stock valuations and executive incentives.

Figure 2.3: Capital flows to the real economy via primary markets, where companies issue new securities (e.g. stocks and bonds); secondary markets are where investors trade existing securities, without directing new funding to companies. Source: University of Oxford

For comparison, the total value of the equity market is much larger than the corporate bond market—outstanding U.S. equities totaled $77.57 trillion in 2023, compared to $10.8 trillion in corporate bonds. But since established companies rarely issue equity, while debt must be renewed regularly, debt markets account for a much larger share of new corporate financing. Between 2009 and 2023, average annual issuance of new equity in the U.S. was $247 billion—roughly one-sixth of the $1.46 trillion raised annually through corporate bonds.

This disparity is especially stark for major emitters: over the past two decades, roughly 90% of all new private-sector financing for fossil fuel companies has come through bonds and bank loans. More than half of the outstanding debt in energy-intensive sectors—including utilities, oil and gas, and autos—is set to mature before the end of this decade, representing about $600 billion in annual refinancing needs. This gives investors recurring, high-leverage opportunities to restrict capital for harmful activities and advance transition-aligned business practices.

Debt and equity financing—across both primary and secondary markets—offer distinct but complementary levers of investor influence. Debt creates regular, time-bound opportunities to intervene through refinancing cycles, while equity provides ongoing governance rights that enable sustained accountability. By focusing on how capital reaches companies and what forms of influence different types of capital provide, investors can tailor their actions accordingly to maximize real-economy impact and reduce systemic climate risk.

Figure 2.4: Corporations raise far more each year through bonds than equity issuances, highlighting the greater and more frequent role investors can play in debt markets. Source: SIFMA

Figure 2.5: Fossil fuel and utility companies raise significantly more capital through debt financing (loans and bonds) than through equity issuance. Source: Ecological Economics

How System-Level Investing Protects Portfolios by Reducing Real-World Emissions

Investors cannot fulfill their fiduciary duties without addressing the systemic risks of climate change. Diversified portfolios depend more on the health of the overall economy than on the performance of individual companies—and economic stability depends on limiting climate damage. Reducing real-world emissions is not outside the purview of institutional investors—it is central to mitigating systemic risk and preserving long-term value.

Yet many conventional strategies—like ESG stock selection and equity divestment—focus narrowly on company-specific risks without confronting the structural drivers of the climate crisis. System-level investing goes further: using financial influence to direct capital flows, reshape corporate incentives, and support policies that accelerate decarbonization—helping protect portfolios from escalating climate impacts.

What follows is an overview of how investors can use each lever of influence—across different types of capital and points of market intervention—to reduce systemic climate risk more effectively than conventional sustainable investing approaches.

Lever #1: Capital Allocation—Steering Financial Flows to Drive Real-Economy Impact

Investors can determine which companies and projects get funding and at what cost. This influence is strongest in primary markets, where firms raise new capital through bond issuances, loans, or stock offerings. Investor decisions at these moments shape whether, and on what terms, funds flow to high-emitting activities or to mitigation and resilience efforts. Redirecting capital at the point of issuance is one of the most effective ways to drive real-economy impact and mitigate economy-wide risk. Denying financing to high-emitting firms without credible transition plans—and scaling investment in climate solutions such as solar, wind, energy storage, and other low-carbon technologies—can strengthen long-term portfolio value. Secondary market trades, by contrast, rarely affect how companies access or use capital.

How investors should use capital allocation to mitigate systemic climate risk:

- Cease new primary-market financing for fossil fuel expansion and restrict capital for high-emitting companies that lack credible transition plans—or fail to follow through. New policies and indices are showing how institutional investors can adopt bond strategies that limit capital flows to companies pursuing new fossil fuel development.

- Condition financing for major emitters on robust decarbonization commitments, ensuring polluting firms put expenditures toward clean energy and sustainable activities. “Transition finance” must be grounded in credible corporate action; investors should be wary of funding that extends the lifespan of polluting assets.

- Scale investments in emissions reductions and climate resilience, targeting industries essential to a low-carbon transition—such as renewable energy generation, grid modernization, building electrification, and clean transportation—guided by credible taxonomies and criteria.

- Apply these principles in private equity and credit markets, even where transparency is often more limited—by setting clear expectations for fund managers, restricting capital to major emitters, and prioritizing investments that enable transition and emissions cuts.

Why this approach to capital allocation is stronger than conventional strategies:

- Primary market capital flows reshape corporate behavior. Investor decisions on new bond and equity issuances directly affect financing costs—raising them for high-emitting firms and enabling climate solutions to scale. While secondary market trades do not provide new funding, capital allocation in the primary market can constrain climate-damaging business models and accelerate real-economy decarbonization.

- Debt markets offer especially powerful leverage. Because most companies refinance regularly, investors have recurring opportunities to deny or condition capital access—especially in capital-intensive sectors like fossil fuels, which rely heavily on bonds and loans to sustain operations and fund expansion. System-level investing targets these flows, where influence is most direct, repeatable, and consequential.

- Redirecting capital accelerates the clean energy transition. Lowering the cost of capital for climate solutions—such as solar, wind, geothermal, and energy storage—helps scale low-carbon sectors, while raising it for polluters reduces their competitiveness. A system-level strategy doesn’t just avoid major emitters—it channels investment into the industries essential for a stable climate and resilient long-term market performance.

Lever #2: Investment Stewardship—Harnessing Ownership to Enforce Corporate Accountability

While capital allocation affects what gets funded, investment stewardship shapes how that capital is used. By owning stocks and bonds, investors retain ongoing influence over corporate strategy and governance. Stewardship tools include nominating and voting on directors, filing and voting on shareholder resolutions, engaging management, and negotiating terms during debt refinancing. Used strategically, these levers allow investors to push companies to align climate targets, transition plans, and capital expenditures with long-term economic stability. More investors must move beyond only demanding transparency—which tends to be the focus of most shareholder advocacy—and prioritize accountability for systemic impacts. This is crucial to driving real-world emissions reductions, not just better disclosures.

How investors should use stewardship to mitigate systemic climate risk:

- Set clear expectations for corporate decarbonization—targeting emissions reductions, capital expenditures, and lobbying activities—and apply a structured escalation process if companies fail to respond.

- Use voting power to enforce accountability—supporting shareholder resolutions and defaulting to votes against directors at high-emitting firms that fail to align with science-based targets. This includes engaging not only with real-economy companies, but also with banks and financial institutions that shape capital flows.

- Leverage bondholder influence during refinancing cycles—pushing for stronger climate terms and potentially declining to roll over debt for high-emitting firms. While bondholders lack voting rights, they can negotiate terms and shape refinancing outcomes to enforce accountability for corporate impacts.

- Collaborate with other investors to strengthen engagement efforts and reduce costs, ensuring companies across sectors face unified, robust expectations for emissions reductions and business model transitions.

Why this approach to investment stewardship is stronger than conventional strategies:

- Shifts from prioritizing disclosure to accountability for systemic impact. Traditional stewardship often emphasizes transparency—pushing companies to disclose how they manage climate risks. But disclosures alone don’t reduce emissions or mitigate systemic threats. Systemic stewardship goes further by holding companies accountable for their climate and market impacts—pushing critical sectors to implement credible transition plans aligned with long-term market stability.

- Maintains leverage to escalate pressure and resist backsliding. Equity divestment forfeits governance rights without limiting access to capital—reducing investors’ ability to influence strategy and demand climate action. By maintaining ownership, investors can use recurring tools like director votes and shareholder resolutions to reinforce expectations. Default votes against directors at major emitters help preserve this leverage while reducing dependence on time-intensive engagement. This approach counters short-term pressures and prevents climate-conscious investors from ceding influence to shareholders who deprioritize long-term stability and systemic risk.

- Links stewardship to capital allocation influence. Systemic stewardship isn’t limited to real-economy firms—it also targets banks, bond issuers, and other financial institutions that fund high-emitting sectors. By using equity and debt ownership to set expectations and enforce accountability, investors can influence not just corporate behavior, but how and where capital gets deployed. This makes stewardship a powerful complement to capital allocation—helping shift financial flows and reinforce economy-wide decarbonization.

Lever #3: Policy Advocacy—Demanding the Conditions for Economy-Wide Progress

While capital allocation and stewardship influence individual companies, policy advocacy enables investors to push for decarbonization across entire sectors and markets. Systemic climate risk cannot be fully addressed without structural reforms that can accelerate emissions cuts. By supporting strong regulations, investors can shape economy-wide transition frameworks—advocacy that’s all the more urgent as government action lags and corporate influence obstructs progress. Investors can affect policy through direct engagement, trade associations, and by holding companies accountable for their lobbying activities. Advocating for strong climate policy is not about partisan politics—it’s about protecting the economic stability on which long-term portfolio value depends.

How investors should use policy advocacy to mitigate systemic climate risk:

- Support enforceable climate policies—such as emissions standards and clean energy incentives—through direct engagement and trade association alignment.

- Push for financial sector reforms that internalize systemic climate risk, including stronger disclosure rules, climate-informed capital standards, and supervisory frameworks that promote market stability.

- Hold companies accountable for lobbying practices, ensuring corporate political spending aligns with science-based climate goals—by supporting mandatory disclosures and using stewardship and capital allocation tools to enforce strong standards.

Why this approach to policy advocacy is stronger than conventional strategies:

- Policy is one of the most powerful levers for economy-wide decarbonization. Capital allocation and stewardship influence companies’ behavior, but public policy can drive emissions reductions at the scale required to protect the global economy. Investors who fail to support strong regulations—emissions limits, clean energy incentives, financial rules, and more—neglect one of the most far-reaching tools to mitigate systemic risk. Investors alone cannot realign incentives without robust government action.

- Fiduciary duty demands action beyond disclosure. ESG-focused advocacy often centers on transparency. But disclosures alone don’t cut emissions or stabilize markets. To mitigate systemic risk, investors must back enforceable policies that restrict pollution, shift financial incentives, and accelerate climate solutions—including sectoral standards, carbon pricing, and public investment in clean technology deployment.

- Investors must counter obstructive corporate lobbying. Major polluters spend billions to delay or weaken climate rules, distorting markets and deepening systemic risk. Diversified investors have a financial interest in challenging these efforts. By advocating for policies that promote long-term economic resilience—not just short-term corporate profits—they help correct market failures and safeguard portfolio value.

Lever #4: Service-Provider Accountability—Elevating Standards for Financial Intermediaries

Many asset owners—such as pension funds, university endowments, and foundations—delegate investment and stewardship responsibilities to asset managers, proxy advisors, and consultants. To manage systemic climate risk and protect long-term portfolio value, they must actively oversee these service providers. That means setting clear mandates to prioritize real-economy impact over firm-level risk avoidance. Without active oversight, asset owners risk ceding control over how their capital is used—and whether it supports or undermines decarbonization.

One emerging example of this dynamic is the trend among some major asset managers—such as BlackRock and State Street—to offer opt-in stewardship options that support climate action. These offerings are limited and insufficient thus far—but the model has important potential. Because large managers serve a wide spectrum of clients, they are less likely to overhaul their entire stewardship approach. But giving asset owners more agency over how their shares are voted opens the door to a broader contest of influence—one in which clients can demand stronger voting policies and better align their capital with systemic risk mitigation. Strengthening and scaling these mechanisms could shift power and increase accountability across the investment system.

How investors should use service-provider accountability to mitigate systemic climate risk:

- Set clear mandates for asset managers, proxy advisors, and consultants to prioritize systemic climate risk mitigation—not just firm-level ESG performance—across allocation and stewardship responsibilities. Investors should also require transparency on engagement activities, voting records, and lobbying positions. This includes leveraging emerging “client choice” proxy voting models to demand and adopt stronger voting policies. These expectations are also critical in private markets, where stewardship tools are limited and alignment must be clearly defined.

- Integrate systemic climate risk into proxy voting guidance, prioritizing long-term market stability over short-term corporate performance. Service providers should recommend votes on directors, resolutions, and governance practices based on companies’ contributions to systemic risk—and demonstrate how their voting guidance aligns with long-term portfolio value and fiduciary obligations.

- Enforce accountability when providers fail to meet expectations—by reallocating mandates, terminating contracts, or publicly signaling dissatisfaction. These strategies reinforce that mitigating systemic risk is a fiduciary duty, not an optional preference.

Why this approach to service providers is stronger than conventional strategies:

- Prevents defaulting to business as usual. Without enforceable expectations, financial intermediaries often focus on short-term benchmarks and narrow ESG metrics—overlooking the broader financial threats of climate change, which are disproportionately driven by some major emitters. Oversight can ensure that allocation and stewardship are tied to real emissions reductions and systemic risk mitigation.

- Reinforces fiduciary duty across the investment chain. Aligning service provider practices with long-term portfolio stability clarifies that fiduciary duty requires more than managing firm-specific risks. Embedding climate accountability into mandates and decision-making helps ensure that managers, consultants, and proxy firms contribute meaningfully to real-economy decarbonization.

In summary: Investors’ levers of influence are most effective when used together to shift financial incentives, redirect capital, and hold companies accountable—essential actions for mitigating systemic risk and protecting long-term portfolio value. That means limiting financing for high-emitting activities, scaling investment in climate solutions, enforcing corporate accountability, advocating for strong climate policy, and setting high standards for intermediaries. System-level risks demand system-level solutions—using financial influence not just to manage company-specific risk, but to protect the health and resilience of the global economy.

While the core case for system-level investing rests on fiduciary duty and long-term portfolio protection, many individuals and mission-driven asset owners—such as foundations, endowments, and faith-based institutions—also aim to align their investments with ethical or reputational values.

Many investors use ESG integration or equity divestment for this purpose, but these strategies primarily decarbonize portfolios rather than reduce real-world emissions. ESG integration is geared toward how sustainability issues affect a firm’s profitability, not its broader impact on society and the economy. And while shareholder divestment can have powerful symbolic effects, it neither deprives companies of capital nor prevents them from raising new funds—and it relinquishes shareholder rights to investors who may prioritize short-term profits over long-term stability.

There’s no universal formula for ethical investing. But climate-conscious investors should ask: is it more ethical to avoid polluters, or to use financial leverage to reduce their harmful impacts? Given the urgency of the climate crisis, the ethical imperative—in addition to the fiduciary duty—is arguably to maximize impacts that lower emissions. That means using the full range of investor levers to shift corporate behavior and financial incentives—not just seeking symbolic alignment with values.

System-level investing offers a framework that is both strategic and principled. It uses financial leverage to accelerate decarbonization, hold corporate polluters accountable, and advance structural changes needed for a livable future. It prioritizes impact over optics—serving investors motivated by both values and long-term performance. By aligning ethical intentions with financially grounded tools for change, investors can reduce emissions more directly—and confront the entrenched power of destructive industries.

Rethinking How to Challenge Social License

System-level investing provides powerful ways to pursue another priority for many mission-driven investors: challenging the social license and political power of major polluters, especially fossil fuel companies. The fossil fuel divestment movement helped advance this goal—stigmatizing the industry’s business model, exposing its policy obstruction, energizing grassroots activism, and pushing institutions to confront their financial ties to fossil fuels. That legacy helped lay the groundwork for many of the financial sector climate strategies emerging today.

Looking ahead, the question is no longer whether to challenge the fossil fuel industry’s power—but how to do so most effectively. Divestment campaigns often aim to weaken companies’ social license by generating public scrutiny and media attention. But reputational impact depends not just on the action taken, but on how it’s perceived, amplified, and interpreted. Visibility, narrative, and symbolic resonance matter—and investors can achieve them through other actions as well. When investors publicly vote against corporate boards or cut off new financing for polluters, they send a clear message about unacceptable behavior. When executed and publicized strategically, these actions can carry just as much reputational weight.

A marquee example came in 2021, when shareholders voted to replace multiple ExxonMobil board members. The campaign generated global media coverage and widespread public discourse—likely matching or surpassing the visibility of many divestment pledges—and demonstrated how shareholder action can elevate scrutiny and drive governance change. While the campaign focused more on Exxon’s capital discipline than on its emissions or systemic impact, it showed that board fights can become flashpoints for public accountability—especially when targeting high-profile climate laggards. The point is not that a company like Exxon can be transformed through engagement, but that shareholder power can spotlight damaging behavior, pressure companies to respond, and drive tangible change.

Crucially, these actions are not one-time events. Unlike equity divestment, which typically reduces or ends an investor’s ownership influence, shareholder voting and new financing decisions can be repeated—at every annual meeting or funding cycle—until demands are met. These recurring moments of financial leverage offer ongoing opportunities to escalate pressure. Investors don’t need to spend excessive time trying to persuade intransigent companies. Instead, they can set clear guardrails—and default to voting against directors who fail to meet them. The Exxon vote showed that investors don’t need to sell their shares to challenge a company’s social standing—they can do so publicly, repeatedly, and in ways that preserve long-term leverage.

The Exxon example also illustrates the risk of failing to sustain pressure. After the initial board shakeup, the lead investor shifted focus, and scrutiny waned as oil prices spiked (following Russia’s invasion of Ukraine)—delivering Exxon and its peers enormous windfall profits. Meanwhile, fossil fuel interests and political allies mounted a broader campaign—under the guise of opposing “ESG”—to attack shareholder rights and sustainable finance. But as history shows, retreating from accountability efforts doesn’t neutralize political attacks—it often emboldens them. The takeaway shouldn’t be that stewardship is futile; it’s that pressure must be sustained, and tied more directly to real-world decarbonization and broader financial stability—which matter most to diversified investors.

System-level investing enables this kind of repeatable, targeted influence through capital allocation and stewardship strategies aligned with structural realities. Investors can challenge corporate power not just through disassociation, but through strategic, steadfast action. The most impactful strategies combine public pressure with financial power—aligning fiduciary responsibility with the moral imperative to reduce systemic harm.

In summary: Ethical investing should be assessed by its ability to mitigate climate damage—not just by avoiding ties to polluters or exposure to firm-level risks. System-level investing uses financial leverage to influence corporate behavior and shift market incentives. It offers effective and repeatable tools for values-driven investors to advance climate action while safeguarding long-term portfolio value.

Conclusion: The Fiduciary Imperative for Climate Action

Climate change threatens global financial stability, yet traditional investment strategies focused on firm-level risks are ill-equipped to address economy-wide impacts. Diversified investors cannot shield portfolios from systemic climate risk by picking stocks, shifting exposures, or waiting for better corporate disclosures. To protect long-term portfolio value, they must take actions that can reduce real-world emissions.

System-level investing offers a more strategic and effective approach. It targets the levers that shape corporate behavior and market dynamics: capital flows, corporate governance, and public policy. Rather than merely adjusting portfolios, it focuses on shifting outcomes in the real economy—where systemic risks originate and must be addressed.

To confront systemic climate risk, investors must strategically apply four levers of influence:

- Capital allocation: Restrict new debt and equity financing for fossil fuel expansion, condition capital access for major emitters on credible decarbonization commitments, and scale investments in the development and deployment of clean energy and other climate solutions.

- Investment stewardship: Enforce accountability for portfolio companies’ emissions, capital expenditures, and lobbying practices. Exercise shareholder voting rights, corporate engagement, and bondholder leverage to drive climate progress.

- Policy advocacy: Support robust climate policies—emissions limits on heavy emitters, clean energy incentives, financial regulations, and lobbying reforms—that drive decarbonization across the economy and strengthen market-wide stability.

- Service-provider accountability: Ensure asset managers, proxy advisors, and consultants integrate systemic climate risk considerations into capital allocation and stewardship mandates—aligning intermediaries with long-term fiduciary responsibility.

Investors cannot fulfill their fiduciary duty—or for many investors, their ethical commitments—without confronting the systemic risks posed by climate change. This isn’t a peripheral concern; it’s central to safeguarding long-term portfolios and global economic stability.

Perpetuating a financial system that defers to corporate self-interest over global prosperity and resilience is no longer tenable. The window to prevent far greater economic and financial harm is closing. To support a stronger, more sustainable economy, investors must prioritize credible impact over symbolic alignment, and use their full influence to accelerate decarbonization—now.

Acknowledgments

This paper benefited greatly from the insight, feedback, and generous exchange of ideas with colleagues and collaborators. I am especially grateful to those who reviewed early drafts, challenged assumptions, and helped sharpen the arguments throughout. Deep thanks to Paul Rissman, Jessye Waxman, Allie Lindstrom, Ginny Roscamp, John Kostyack, Adele Shraiman, Rick Alexander, Jeremy Fisher, Mahima Dave, Ada Recinos, Jon Lukomnik, and Keith Johnson. Their thoughtful engagement played a key role in shaping the final product, though any remaining shortcomings are my own.

This paper also builds on the research, expertise, and thought leadership of many others who have advanced the field of sustainable finance. While I cite a number of them throughout, there are undoubtedly many more whose work has influenced my thinking and helped make this possible.

Disclaimer

This publication is provided for informational and discussion purposes only and does not constitute investment, legal, tax, or other professional advice. While efforts have been made to ensure the accuracy and reliability of the information contained herein, no representation or warranty is made as to its completeness or suitability for any particular purpose. The author and the Sierra Club expressly disclaim any liability for any loss or damage arising from reliance on this publication. Readers should seek independent professional advice as appropriate.