The fossil fuel industry in the United States is being crushed under the weight of its own debts, laden by years of speculation that consumers would someday be willing to pay a premium for carbon-intensive fuels. Some producers are seeing a reckoning around the corner, while other producers are already facing bankruptcy today. An independent law firm tracked 36 oil and gas producer bankruptcies in the first eight months of 2020 alone, putting $51 billion of debt at risk.

The financial woes of oil and gas producers have the potential to leave the United States with a legacy of unplugged wells and an overwhelming cost to close those wells. In a recent study, CarbonTracker, a financial think tank, estimated that plugging the known 2.6 million onshore oil and gas wells in the United States could cost upwards of $280 billion.

Why do we care about unplugged wells? Open well bores are a pathway from oil and gas to groundwater, the surface, and the air. Wells tend to leak methane, a potent greenhouse gas -- but wells that aren’t being used for production tend to go uninspected and degrade, can be substantial sources of methane, and can contaminate surface soils and waters. The EPA estimates that the US has more than three million abandoned, unplugged wells.

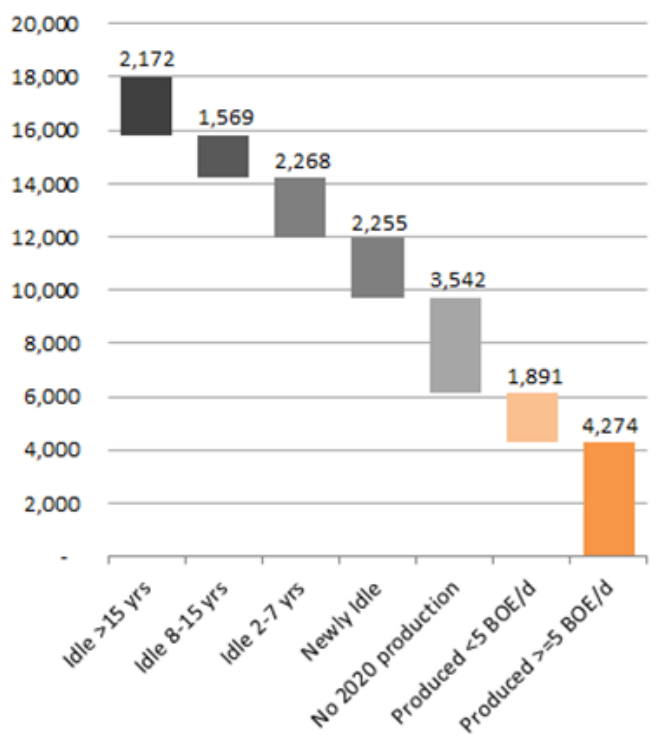

So how far out is that risk actually? In our new study of the now bankrupt California Resources Corporation (CRC), we estimate that there is a very high likelihood that the state will end up paying for that private company’s $900 million worth of closure obligations if it doesn’t take corrective actions quickly. Today CRC is sitting on nearly 18,000 wells, the vast majority of which have either been sitting idle for years, haven’t produced at all in 2020, or produced only a trickle of oil (less than five barrels of oil per day). Our study shows that CRC won’t be able to cover its own closure costs given its dismal performance and the current projections of oil and gas prices.

CRC declared bankruptcy in mid-July 2020, blaming its financial woes on the debt on its books, and its inability to create steady returns. We assess that even after the company restructures its debt, it still won’t be able to produce profitably, earn enough income to pay down its debt, and meet its closure obligations. At the end of the day, CRC will go bankrupt again, and the next time it will make its mess of wells a ward of the state - and state taxpayers.

CRC is just the proverbial tip of the iceberg in California. The state has over 114,000 unplugged wells, and 39,000 are idle -- a term the state reserves for wells that haven’t produced in two years or more. And as with CRC, only a small fraction of California’s wells are actually producing in quantities that might support their continued operations.

Less than 20 percent of California’s oil and gas wells are producing more than five barrels of oil per day, meaning that the vast majority are sitting idle, or are near idle

CRC: Occidental’s Dumping Ground

CRC is a new company holding some very old wells. In 2014, Occidental Petroleum, one of the largest oil producers in the US, spun off CRC, bequeathing the new company all of its legacy oil and gas wells in California. Interestingly, while CRC was created as a corporate entity in mid-2014, Occidental spun off CRC at the end of 2014, in the middle of the second-sharpest downturn in oil prices in recent history.

At the time, observers noted that the spinoff was meant to “address investor concerns that Oxy's California operations cost the rest of the company too much money without producing enough return on that investment.” Even in 2014, Occidental saw that its operations in California were going to be a drag.

And of course, that’s exactly what happened. In its bankruptcy declaration, CRC blames its state of affairs on a “late-2014… diminished asset base compared to CRC’s initial debt burden.” In other words, it was clear from the start that CRC wouldn’t be able to generate sufficient revenues to be able to satisfy its debts.

CRC’s Outstanding Obligations

As CRC goes bankrupt, it is sitting on nearly 18,000 wells. And the majority of those wells are not productive. According to the company’s reporting to the state, two-thirds of the company’s wells produced nothing at all in 2020 or have been sitting idle for years or decades. Only about a quarter of the company’s wells produced enough oil to be considered “productive” at more than five barrels of oil equivalent per day.

About two-thirds of the wells operated by California Resources Corporation are either idle (i.e., haven’t produced in two years or more) or haven’t yet produced any oil or gas in 2020.

That’s a hard space to be in when you want to generate enough cash to pay back several billion in outstanding debt and also need to start closing wells.

So how much does CRC have in outstanding closure obligations? Using estimates from a recent state report, we project that CRC faces nearly $900 million in closure obligations for its 18,000 wells. That closure obligation makes it the second-largest outstanding liability faced by CRC -- and one that it cannot discharge.

No Clear Path to Recovery

CRC’s bankruptcy is a restructuring. It’s meant to allow the company to shed much of its debt and try to stay afloat as a company. To get there, CRC has proposed to jettison its shareholders (i.e., they’ll be left with nothing) and pay pennies on the dollar to the debtors who were second in line. Nonetheless, the company will still hold substantial debt after the restructuring and will need to generate cash to pay its interest expenses, eventually pay off that debt, and meet its closure obligations.

That’s where CRC runs into a problem. Right now, the company’s day-to-day operations cost just about as much as it can get by selling oil and gas. And the price of oil isn’t really going up. After taking a dive earlier in 2020, forward prices are holding at about $40/barrel and rising slowly. Take away all the extra financial derivatives, hedges, and swaps, and what you’re left with is a company that’s projected to make no net revenues. That means no money to pay off its debts and no money to pay off its closure obligations.

And there are other obstacles. The company has been using enhanced oil-recovery techniques (like steamflooding) for the last few years in an attempt to squeeze a few more drops from some of its wells. But while those techniques enhance production up front, they deplete the company’s wells that much faster. Our analysis of the company’s decline rate, or how quickly its wells are decreasing in productivity, is likely conservative because of the use of steamflooding. In reality, the company’s wells are declining much faster than we’ve modeled -- which means CRC will run out of cash that much faster.

We project that, accounting for CRC’s closure obligations, the company will end up in a deeper and deeper hole year by year. And when the company’s debts next come up for refinancing, potential creditors will look for better prospects elsewhere.

California’s Uncomfortable Position

So if the prospects for CRC are so dismal, why are banks backing the bankruptcy reorganization instead of just taking their money and running? Some of CRC’s creditors may be placing bets on an oil recovery, but others might have noted that the bankruptcy plan stays eerily silent on the topic of the company’s closure obligations to the state of California. Hoping the state will be lax in its enforcement of closure obligations might give CRC’s creditors the confidence to write down, or dismiss, at least that obligation. And in fact, the state appears to have stayed silent on the bankruptcy, despite a plea from environmental organizations.

CRC relies on California’s lax enforcement of its closure obligations to leave idle wells unplugged. Normally, an operator should move to close oil wells that have ceased producing relatively quickly -- doing so allows the operator to plug before the well starts to deteriorate, prevents leakage into groundwater and the air, and ensures that the operator has enough money on hand to close its own well.

But California’s closure obligations are some of the loosest in the country, allowing wells to sit idle for 15 years or more (and indeed, more than 2,200 of CRC’s wells have done just that). And while California requires that operators of long-idle wells submit plans to close those wells, those plans are not public.

But don’t producers have to hold bonds to secure the cost of closure? The answer is complicated, but amounts to “barely.” California allows for “blanket bonds,” a process by which an operator with a large number of wells simply has to hold a single bond that is meant to cover all of its wells. In CRC’s case, it is required to hold a $3 million bond… to cover its $900 million obligation. The concept of a blanket bond never envisioned whole industries suffocating under debt loads.

Salvaging a Bad Situation

California has a few options still to ensure that it isn’t left holding the proverbial bag. Rapid and decisive action might even forestall the impending game of well-closure hot potato.

- The state should make sure it has a bankruptcy remote vehicle to secure CRC’s obligations. The state could require a trust or a much larger surety bond that specifically carves out the closure funds. CRC could draw down that trust to close its wells -- but only for that purpose, ensuring that the state has a pool of cash irrespective of CRC’s fortunes.

- California should be prepared to pursue Occidental for any monies it can’t collect from CRC. When Occidental spun off CRC, it was attempting to shed those liabilities. California should evaluate its legal remedies against the initial parent company.

- The state should sharply increase its closure obligations and timelines, and stop extending closure requirements in hopes that eventual price recoveries will fund the plugging and abandonment obligation. By keeping extended closure deadlines, California is enabling bad behavior.

- The state should increase its bonding obligations for all wells to ensure that it has adequate coverage when its other producers start slipping.

- California should tie permitting to closure. There should be no circumstances where an operator with a backlog of unclosed idle wells is being granted the ability to drill new holes in the ground.