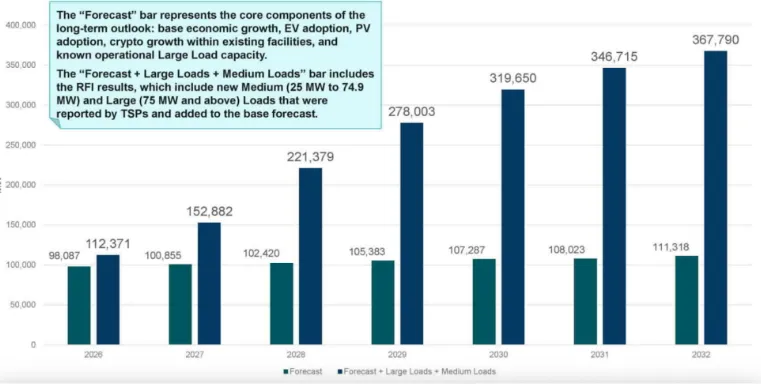

Last month, ERCOT made a startling mid-term projection: total demand could go from roughly 90 GWs of power in 2025 to 367 GWs of demand by 2032.

This is if all the proposed data centers, AI facilities, crypto-mines, and other medium and large industrial loads came on-line. Realistically of course, not even ERCOT believes that 367 GWs of total demand could be on our system in 2032 because we don’t have either the generation to provide that level of power nor the transmission capacity to move that amount of power around the state, but it is still a startling “what if” prediction. So how does ERCOT predict the short, medium and long-term demand for Texas’s main electric grid, and how do we plan all the transmission needed to serve that load? And who ultimately pays for it?

How ERCOT Predicts Future Demand (and Supply!)

As a reminder - ERCOT - the Electric Reliability Council of Texas - is the independent grid operator of Texas that is tasked with assuring that the supply of electricity can meet the demand of electricity, the grid operates smoothly, and whatever transmission is needed to move those electrons around gets built. They don’t own any transmission, or generation and they don’t sell any electricity that’s all private (and sometimes public) industries, but they are charged with setting up the rules and managing it all. Above them, the Public Utility Commission of Texas is the ultimate authority.

To do this, they have to look into their crystal ball and see if they can match supply and demand and assure the lines are there to carry those electrons. They have both short-term and long-term tools.

Monthly Outlook for Resource Adequacy

Looking at more short-term needs, ERCOT publishes a monthly report that uses information to assure that the existing electricity supply - including new power plants just coming online - will be there to meet demand. First, a relatively new tool that arose after the disastrous Winter Storm Uri event of 2021, ERCOT publishes the MORA - Monthly Outlook for Resource Adequacy – on the first Friday of each month, and the report looks out at the upcoming month and assesses whether supplies will be there to meet the needs, including in an extreme weather event which tends to drive up demand.

As an example, the July MORA which was just released shows a very tiny chance - 0.21% - that ERCOT could issue an Emergency Energy Alert (when the system falls below a certain amount of electricity) on a summer evening hour, but that’s only if wind is very low and the storage that normally kicks in the summer evening is unavailable. There is even less chance that ERCOT could order rolling outages - like a 0.11% chance. While ERCOT used to produce a SARA - the Seasonal Assessment of Resource Adequacy - the MORA was viewed as more useful for the day to day operations of the market.

For this short-term analysis, ERCOT only looks at existing supply resources (and some demand-side resources like demand response) to figure out if we will have reserves.

Capacity, Demand and Reserves Report

The CDR - or Capacity, Demand and Reserves Report - has been around for decades but was recently revised to provide a more nuanced look at how planned new generation is keeping up with increasing demand over the next five years. The report is released in May and December, although in 2026, ERCOT is skipping the May report because of an upcoming ERCOT study of large loads known as the “Batch Zero Study” which is not expected to be completed until late in the summer and will influence what demand projection is included in the CDR for the next five years.

It’s important to note that the CDR can change substantially from one report to another as planned generation resources can either hit a roadblock or be approved for interconnection from one cycle to the next, as can new large loads like data centers if they are approved by a local interconnection for interconnection. Put simply, predicting demand and supply is a lot easier to do a month from now than five years from now but importantly the CDR does provide a look at how the grid might operate under normal conditions, or extreme weather events, providing an important planning tool for the future.

December 2025 CDR

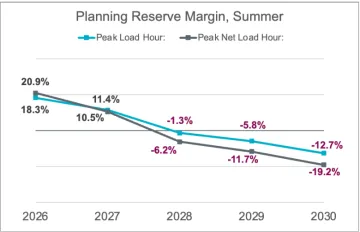

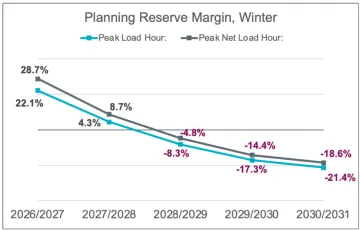

While somewhat outdated, the December 2025 CDR shows real concern for not being able to maintain sufficient reserves beginning in 2028 due to the large amount of large loads wanting to interconnect to the ERCOT grid. However, the CDR doesn’t really predict the future but shows under differing scenarios how the ERCOT grid might perform, using both potential new generation resources and new demands. ERCOT makes assumptions on what generation resources will be built based on whether they meet certain “planning” criteria, such as whether they have an interconnection agreement or whether they have posted financial assurance. Thus, the future supply is an educated guess.

The base scenario in the December 2025 CDR—using "Protocol Prescribed" capacity resources and the ERCOT Adjusted Load Forecast—indicates that summer and winter Planning Reserve Margins for 2026 through 2030 decrease significantly from year to year, and cross over to negative values in 2028 in line with the trends reported in the May 2025 CDR. The base scenario's summer 2026 Planning Reserve Margins are 18.3% for the peak Load hour (Hour Ending 5:00 p.m. Central Standard Time). However, as the graph indicates below, because the Legislature passed a major piece of legislation in 2025 dealing with interconnecting large loads, the actual amount of loads that will interconnect is likely to be much lower than those wanting to interconnect, hence the different scenarios. Thus, while it is very likely that “reserves” will shrink, just how much depends in large part on which large loads meet new rules on interconnection yet to be finalized at the PUCT. In fact, because of this uncertainty, ERCOT decided not to release a May 2026 CDR and to wait until rules, and the so-called “Batch Zero” study is finalized in August or September of this year. Thus, it is widely expected that the CDR later this year will show less issues than the one issued last December. Put simple, all the assumed loads will not be approved to interconnect.

Long-Term Demand and Energy Forecast (LTDEF)

The CDR is based in part on ERCOT’s load forecast. Known officially as the Long-Term Demand and Energy Forecast (LTDEF) the LTDEF is comprised of six forecast components: Economic Base Load Forecast, Electric Vehicle Forecast (EV), Behind the Meter Rooftop Photovoltaic Forecast (PV), Large-Flexible Load Forecast (LFL), Large Load Contracts, and Large Load Officer Letters. The LTDEF combines each forecast to create the ERCOT Net Forecast. However, because of concern about how “Large load officer letters” and “Large Load Contracts” include uncertainties with the advent of new AI and data centers in particular, ERCOT’s 2026 LTDEF came basically with an asterix - ERCOT itself didn’t trust its own forecast of 367 GWs by 2032. In fact, even their prediction for 2026 itself - up to 112 GWs of power de- is, they admitted, very unlikely, and they instead have already adjusted it to a range between 90 and 98 GWs.

In terms of generation, the ERCOT queue of power plants interested in coming on-line is large, mainly from battery storage, solar and gas. While there are also some wind projects, delays imposed by the Trump Administration on permits from the Department of Defense has made wind development more difficult. The Table below shows the amount of new generation expected to come online over the next two years.

ERCOT Generation Queue: New Resources Expected to Come On-line within three years

Note: *These wind contracts are subject to delay because of Trump Administration delays on permits from military.

** Several coal plants have announced they expect to retire units between 2027 and 2030. However, until there is an official announcement of retirement we are not showing those declines.

*** Several small modular nuclear reactors have been announced but none have interconnection agreements to serve the ERCOT market.

Distributed Energy Resources

It’s important to note that there is another source of resources that Texas has not taken full advantage of. Distributed energy resources like onsite solar and battery storage are growing in Texas. Currently, ERCOT is reporting that there are some 3,217 MWs of “unregistered” Distributed Generation resources - onsite mainly solar generation - currently on-line within the ERCOT market, but ERCOT does predict that amount could double over the next three to five years as customers seek more control over their energy bills. Another huge opportunity is in demand reduction, through reducing energy waste, energy savings programs and programs that shift electric demand from peak periods to other periods, sometimes known as “demand response” programs.

While Texas does require private utilities like Oncor and CenterPoint Energy to run energy savings programs, Texas’s goals and achievements are relatively low compared to most states. The Sierra Club has advocated for years to increase our utility goals to reduce energy use from roughly 0.20 percent of load today to one percent of overall load by 2030, but thus far neither the legislature or PUCT has made major changes to the programs. Sierra Club is working with some utilities to increase their budgets for these programs in 2027 but more should be done to help residential consumers reduce their total energy consumption, especially during peak use times. Recent reports suggest there are literally thousands or even tens of thousands of MWs of demand reduction and energy waste reduction available in our system with the proper investment.